The median price per square foot in the Coachella Valley was unchanged in January at $180. However, seven of the valley’s nine cities had higher prices, which shows the limitations of using only statistics when pricing the housing market — especially over smaller geographical areas.

Since we’re discussing home prices, we should give the Market Watch 2015 price forecast for the valley. The projection is simple: It depends almost completely on the banks.

If banks don’t start easing up on their tight credit requirements, our general forecast is that prices will be essentially unchanged. However, if they do ease up, we think a further price increase of 10 percent is possible. It simply comes down to increasing buyer demand to offset rising inventory.

Banks Need to Qualify More Home Buyers

If this housing recovery is to continue, banks must start qualifying more home buyers. Too many applicants are being declined unnecessarily because of abnormally high credit requirements. Most of this is due to confusion over the new Fannie Mae and Freddie Mac regulations about bank liabilities in the new housing world. The agencies have not clearly defined exactly what these liabilities are. The agencies must spell out and clarify in detail what the new bank risks are before the banks can become comfortable lending to applicants with lower — but still safe — FICO scores.

Inventories Are Starting to Rise

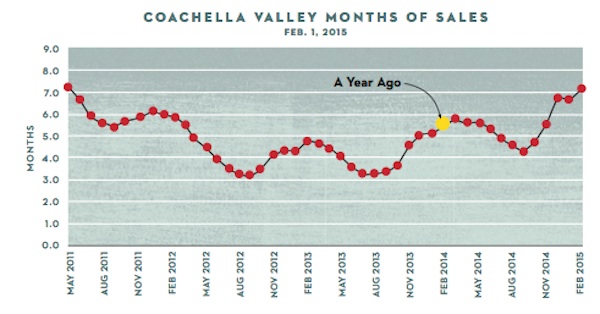

We are finally beginning to see the negative effect tight credit is having on our market: It’s causing inventories to rise. The inventory as of Feb. 1 stood at 5,000 units; a year ago it was 4,000. That’s a 25 percent increase. When inventory is divided by the sales rate, you get an important ratio called “months of sales.” On Feb. 1, it was 7.2 months; a year ago, it was 5.5 months (see chart). This change is significant because six months is often considered the dividing line between a healthy market and a weak one, as months of sales is an indicator of how long it takes to sell a home. History shows that if it exceeds six months, sellers often get nervous at the inactivity and begin to lower asking prices to get movement.

Some of this is the seasonal pattern in the desert. As history and the chart show, inventory and months of sales usually peak sometime between February and March, when sales begin to pick up. It will be vital to follow these metrics closely to see if the ratio can again get below six months by early summer. This situation just reiterates why banks must begin to loosen credit requirements. It really is a race between finding more buyers before the rising inventory begins to push prices down.

High-end Market Looks Favorable

We should state that this situation does not apply to homes selling for more than $1 million. Seventy-five percent of the homes in this price range are second homes, and these purchases are often cash buys; credit is not an issue. The decision to buy depends primarily on buyer net worth, and if you’ve been following the stock market lately, you’ll know the net worth of this class of buyer is currently going through the roof.

Vic Cooper and Mike McDonald are partners in Market Watch LLC, a nationally recognized real estate advisory firm that publishes The Desert Housing Report; www.marketwatchllc.com

Save the Date

Want to find out what’s happening in the valley’s high-end housing market? Attend our next Market Watch seminar, Wednesday, April 22, from 8 to 10 a.m at Villa Portofino in Palm Desert. Visit www.palmspringslife.com/marketwatch for more information.

Sponsored by